Fixing the Fixes? Approach to Merger Remedies Changing Under New Political Regimes

The antitrust enforcement regimes in the United States, the United Kingdom, and the European Union are in various stages of political turnover. We are only beginning to learn what practices may continue from the recent past and what may change, but antitrust enforcers’ approaches to merger remedies appears to be a key area of reconsideration. In particular, senior officials from the U.S. antitrust agencies have made public statements about their renewed openness to merger settlements through formal consent agreements, and there have been concrete examples of this policy in action in Synopsys, Inc./Ansys, Inc., Keysight Technologies Inc./Spirent Communications plc., Safran S.A./Collins Aerospace, and Omnicon/IPG. At the same time, the UK Competition and Markets Authority (CMA) has published an open consultation on its approach to merger remedies, having signaled a willingness towards more flexibility going forward.

Despite this new openness, competition agencies may diverge on the types of remedies they are willing to consider. In this post, we examine recent developments on both sides of the Atlantic and the impact they could have on deal planning.

The Biden Administration’s Aversion to Approving Merger Settlements

Historically, whenever possible, the U.S. antitrust agencies would approve merger settlements in consent decrees to resolve competitive harm posed by transactions. However, the Biden Administration took a strong stance against merger remedies, preferring to challenge transactions outright rather than resolve competition concerns through negotiated consent agreements. Facing the threat of litigation, merging parties sometimes pursued their own divestiture agreements or behavioral commitments (known colloquially as “fix-it-first”). In some instances, these fix-it-first remedies did not deter the U.S. antitrust agencies from pursuing court challenges. In other instances, the remedy sufficiently impaired the agencies’ litigation cases, so the agencies opted not to give these fix-it-first remedies the imprimatur of government approval, and allowed transactions to proceed without consent decrees.

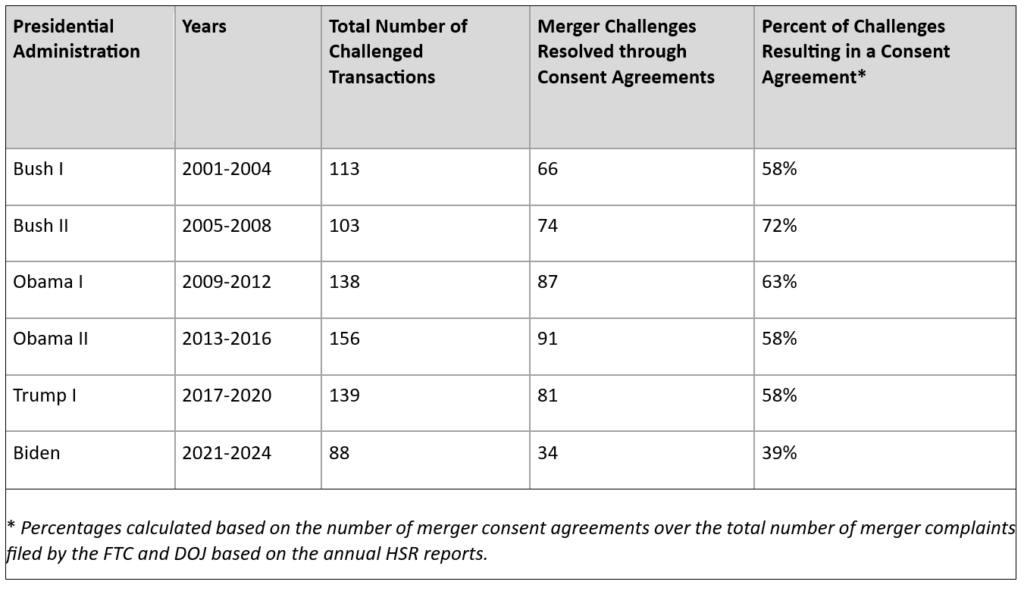

While previous administrations typically pursued consent agreements in the majority of merger challenges, the approach of the Biden Administration led to a drop in such agreements from 2021-2024. Even excluding the “fix-it-first” remedies that resulted in no agency action, only 39% of merger challenges were resolved by consent agreements under the Biden Administration, compared to an average of over 60% during the previous two decades.

Second Trump Administration Appears Poised to Revive Consent Agreements

In a significant break from the past administration, both Gail Slater, head of the DOJ’s Antitrust Division, and Andrew Ferguson, Chairman of the FTC, have stated that they will be more open to considering remedies to resolve merger concerns than their predecessors. Both leaders noted that remedies can successfully restore competition. The agencies’ recent settlements to resolve the Synopsys/Ansys, Keysight/Spirent, and Safran/Collins Aerospace transactions align with these policy statements. On May 28, 2025, the FTC announced that Synopsys and Ansys will divest assets across three software tools markets to resolve antitrust concerns with their merger. Just a week later, the DOJ announced it will require Keysight Technologies (coincidentally, the divestiture buyer in Synopsys/Ansys) and Spirent Communications to divest network and network equipment testing businesses to remedy competition issues from their deal. More recently on June 17, 2025, DOJ ordered Safran to divest its North American actuation business, which DOJ alleged competes head-to-head with RTX’s Collins Aerospace subsidiary, to Woodward in order to proceed in its acquisition of Collins.

In both the recent statements and consent agreements, the DOJ and FTC focused on structural remedies (i.e., the divestiture of businesses or assets to maintain the pre-merger market structure) rather than behavioral remedies (i.e., commitments by merging parties to act in a certain way to avoid anticompetitive effects of the merger). In the FTC’s statement on Synopsys/Ansys, Chairman Ferguson, joined by Commissioners Holyoak and Meador, stated that the Commission “should accept settlements in merger cases only when it is confident that the settlement will protect competition in the relevant market to the same extent that successful litigation would.” The statement cautioned against “uncertain settlement” that does not guarantee a solution to the claimed competition problem, and he noted that the FTC will entertain behavioral remedies with “substantial caution” as they can be “difficult or impossible for the Commission to enforce effectively,” especially where they “lock the Commission into the status of a monitor for individual firms rather than a guardian of competition across the entire economy.”

DOJ’s statement accompanying the Keysight/Spirent merger also focused on the structural aspect of the remedy: “This structural solution preserves competition [and] secures enforceable commitments from the merging parties, provid[ing] transparency into the Antitrust Division’s efforts to resolve merger investigations.” Deputy AAG Bill Rinner also recently commented that the Keysight/Spirent settlement exemplified the DOJ’s continued preference for “strong, robust” structural remedies that “provide great confidence in their ability to protect competition.”

Likewise, in DOJ’s statement announcing the divestiture in the Safran/Collins deal, AAG Slater described the settlement as “a structural solution to an acquisition that would have harmed competition” which “ensures that American customers will continue to benefit from competition, and the incentives of Woodward, the merging parties, and their customer base are aligned with the remedy’s success.” AAG Slater’s statement highlights the value DOJ places on the enforceability of structural settlements.

Despite the agencies’ stated preference for structural remedies, the FTC recently accepted a behavioral remedy in a consent agreement to resolve concerns that the Omnicon/IPG transaction threatens to further consolidate the U.S. media buying services market. The behavioral remedy requires that Omnicom not engage in any collusion or coordination to direct advertising away from media publishers based on the publishers’ political or ideological viewpoints. Chairman Ferguson issued an accompanying statement, noting that due to the “history of collusion in the market for media-buying services, and the increased potential for collusion post-merger” this is “a rare instance where the imposition of a behavioral remedy is appropriate.”

These statements and early agency actions should provide merging parties with increasing comfort that they can once again plan for merger clearance with agency-approved remedies.

Major Changes Ahead in the UK: Increased Openness to Behavioral Remedies?

The UK Competition and Markets Authority has traditionally shared the U.S. agencies’ preference for structural measures to resolve competition concerns. In recent months, however, the CMA has signaled that it will be more flexible in considering different solutions put forward by merging parties.

In her November 2024 speech, Sarah Cardell, the CMA’s Chief Executive, indicated that “every deal that is capable of being cleared either unconditionally or with effective remedies should be.” As we have discussed previously, this speech previewed the announcement of major reforms of UK merger control in February, focused on improving pace, predictability, proportionality, and process in support of the UK government’s pro-growth agenda. This was followed by the launch of a review of the CMA’s approach to merger remedies in March.

The CMA has now completed an initial consultation, seeking input from stakeholders on a number of broad themes, including the key principles that the CMA applies in assessing the suitability of potential remedies under its existing guidance (particularly “how the CMA can best reflect the need for proportionality in its consideration of remedies”), how remedies can be used to preserve merger benefits by locking in efficiency commitments, and how the CMA’s processes for assessing remedies could be improved (for example: giving “the greatest possibility” of accepting phase 1 remedies to avoid a phase 2; improving the assessment at phase 2 to more quickly reach evidenced-based decisions; and effectively taking account of parallel actions by other competition authorities when deciding whether a UK remedy is needed) . The CMA is specifically reconsidering its approach to behavioral remedies. In particular, the review will consider whether the current distinction between structural and behavioral remedies remains “helpful and meaningful”, the circumstances in which behavioral remedies may be appropriate to resolve potential concerns, and how the CMA should assess their effectiveness.

The CMA’s clearance of the Vodafone/Three UK joint venture in December 2024 signaled a greater openness to behavioral remedies. This 4-to-3 mobile merger was cleared subject to a novel “investment remedy” whereby the merging parties committed to roll out a joint network plan that sets out the network upgrade, integration and improvements the parties will make to their combined network across the UK over the next 8 years. It also requires the merged entity to cap certain mobile tariffs and offer specific contractual terms to mobile virtual network operators for three years. The CMA has indicated that its revised guidance will build on the approach taken in Vodafone/Three UK to design remedies that lock in merger-specific efficiencies and preserve customer benefits, and may broaden the circumstances in which the CMA is likely to accept behavioral remedies.

The CMA has stated it will now develop specific proposals for further consultation in the early autumn, with a view to implementing changes by the end of 2025.

The European Commission Remains Open to Behavioral Remedies

A more open stance towards behavioral remedies would bring the CMA’s approach more in line with that of the European Commission (EC), which has in recent years showed more willingness to accepting behavioral or quasi-behavioral solutions, particularly involving licensing commitments (including in horizontal mergers, such as in Mastercard/Nets). The EC is not publicly planning any reforms to its remedies toolkit at this stage, and it remains to be seen whether the recent the appointment of Teresa Ribera as Commissioner for Competition and Executive Vice-President for a Clean, Just and Competitive Transition will bring any shifts in the EC’s approach to remedies in practice. The EC, however, has announced a review of its horizontal and non-horizontal merger guidelines. In Ribera’s words, this review aims to ensure, among other things, that “innovation, resilience and the investment intensity of competition in certain strategic sectors are given adequate weight in light of the European economy’s acute needs”. This review may well lead to a reexamination of merger remedies if Commissioner Ribera looks to broaden the EC’s competition toolkit.

Looking Ahead

Antitrust regulators’ openness to merger remedies worldwide is a positive development for dealmakers. The U.S. antitrust agencies appear likely to reinvigorate the use of consent agreements to formalize structural merger remedies, potentially providing greater leeway to speed up investigations, avoid costly litigation, and bring more predictability back to M&A. In its statement on Synopsys, Inc./Ansys, Inc., the FTC indicated that the Commission would publish a policy statement “on its understanding of the role of remedies” in due course, with the potential to bring even more transparency to this space, including as to acceptance of behavioral remedies.

Meanwhile, the UK CMA’s apparent increased openness to behavioral remedies may ultimately bring it more in line with the EC. As a result, the landscape for global mergers continues to be highly complex and potentially requiring multiple remedies tailored to specific jurisdictions. This highlights the importance of dealmakers giving early consideration to potential remedies and developing a coordinated, global strategy for agency engagement.

* Joela Qose contributed to the content of this post.

Contributor(s)

More from the WorthWeil Antitrust Blog

Copyright © 2026 Weil, Gotshal & Manges LLP, All Rights Reserved. The contents of this website may contain attorney advertising under the laws of various states. Prior results do not guarantee a similar outcome. Weil, Gotshal & Manges LLP is headquartered in New York and has office locations in Austin, Boston, Brussels, Dallas, Frankfurt, Hong Kong, Houston, London, Los Angeles, Miami, Munich, New York, Paris, San Francisco, Silicon Valley and Washington, D.C.